{kind=link}

Understanding your financial health requires more than just looking at the total value of everything you own. While many people focus exclusively on their total net worth—which includes illiquid assets like real estate, vehicles, and collectibles—the most critical metric for navigating day-to-day life and emergencies is your Liquid Net Worth. By isolating assets that can be quickly converted into cash without a significant loss in value, you gain a clearer picture of your immediate financial security and your ability to pivot when life throws an unexpected challenge your way. This article breaks down why this metric matters, how to calculate it, and why it is the true engine of your financial freedom.

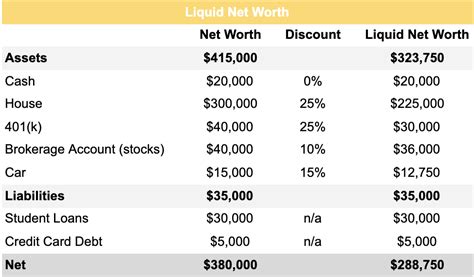

What Exactly Is Liquid Net Worth?

At its core, liquid net worth represents the sum of all your cash and cash equivalents minus your short-term liabilities. Unlike total net worth, which may include assets that take months to sell—such as a home, a business, or high-end art—liquid assets are designed to be accessed with minimal effort or delay. Essentially, if you needed to pay off a major expense tomorrow, these are the assets you would rely on.

The distinction is vital because liquidity provides optionality. If all your wealth is tied up in a house, you are "asset rich but cash poor." If you lose your job or face an emergency, you cannot easily pay for groceries or mortgage payments using a fraction of your kitchen wall or the equity in your home. Maintaining a healthy balance of liquid assets ensures that your financial life is not held hostage by the pace of the real estate or secondary markets.

Assets Included in Your Liquid Net Worth Calculation

To determine your figure, you must distinguish between what is truly "liquid" and what is merely "valuable." Liquid assets must be convertible to cash within a very short timeframe—ideally a few days or less—without significant price concessions. Common examples include:

- Cash and Checking Accounts: Money immediately available for use.

- Savings Accounts: High-liquidity accounts that usually offer a small amount of interest.

- Money Market Accounts (MMAs): These often offer slightly better rates than standard savings while maintaining liquidity.

- Certificates of Deposit (CDs): While they have maturity dates, they can be liquidated early (usually with a minor penalty).

- Stocks, Bonds, and ETFs: Assets traded on major exchanges are highly liquid, as they can be sold during market hours and settled within a few days.

- Mutual Funds: Generally considered liquid, though it may take a day or two for the transaction to finalize.

Items such as physical real estate, private business equity, jewelry, or classic cars are not included in this calculation because they lack the "instant access" requirement that defines true liquidity.

How to Calculate Your Liquid Net Worth

Calculating this figure is a straightforward process. You are essentially creating a snapshot of your "spendable" wealth. Follow this simple formula to find your number:

(Cash + Cash Equivalents + Marketable Securities) - (Short-Term Liabilities) = Liquid Net Worth

To give you a better idea of how different assets and liabilities stack up, refer to the table below:

| Category | Description | Liquidity Status |

|---|---|---|

| Checking/Savings | Cash on hand | High |

| Public Stocks | Marketable securities | High |

| Primary Residence | Real estate equity | Low (Illiquid) |

| Credit Card Debt | Current liability | Negative Impact |

| Private Business | Ownership stake | Low (Illiquid) |

💡 Note: When calculating your liabilities for this specific metric, focus on debts that require immediate or near-term payment, such as credit card balances or personal loans, rather than long-term, fixed-interest debt like a standard 30-year mortgage.

Why Investors Prioritize Liquid Assets

The primary benefit of prioritizing liquid net worth is the reduction of financial stress. When your wealth is locked away in assets that require lengthy sales processes, you are vulnerable to market timing. If you are forced to sell a home during a market downturn just to cover an emergency, you lose significant value. By contrast, a robust liquid portfolio acts as a "buffer zone."

Furthermore, liquid assets provide the capital agility needed for wealth creation. When investment opportunities arise—such as a market correction where high-quality stocks become undervalued—having liquid capital allows you to take advantage of those moments immediately. Those who lack liquidity must sit on the sidelines, watching wealth-building opportunities pass them by while they wait for other assets to sell.

Strategies to Enhance Your Liquidity

If you find that your net worth is heavily skewed toward illiquid assets, you may want to rebalance your portfolio. Start by building an emergency fund that covers 3 to 6 months of living expenses in a high-yield savings account. This is the cornerstone of your liquid portfolio.

Once your emergency fund is stable, consider diversifying your investments into liquid vehicles like index funds or ETFs. These allow for long-term growth while maintaining the flexibility to sell portions of your holding if circumstances change. It is also wise to avoid over-leveraging; if you have significant debt, prioritize paying it down to reduce your monthly liability burden, which effectively increases your "net" position by freeing up future cash flow.

Regularly reviewing your financial statement is essential. Aim to perform a "liquidity audit" at least once or twice a year. During this time, look at your debt-to-income ratio and assess whether your cash-to-asset ratio is sufficient to meet your long-term goals and short-term peace of mind.

💡 Note: Always consider the tax implications before liquidating assets. Selling stocks in a taxable account may trigger capital gains taxes, which should be factored into your decision-making process.

Balancing Total Net Worth vs. Liquid Net Worth

It is important to emphasize that neither total net worth nor liquid net worth is "better" than the other; they serve different purposes. Your total net worth is a scorecard for your long-term wealth accumulation and retirement planning. It tracks whether you are getting wealthier over time through investments in appreciating assets like real estate or equity in a business.

However, your liquid net worth is your tactical dashboard. It tells you whether you are prepared for the "here and now." A successful financial strategy involves growing your total net worth while ensuring that a sufficient percentage—determined by your risk tolerance and lifestyle needs—remains liquid. Finding this equilibrium is the hallmark of a mature and stable financial strategy. By maintaining a focus on accessibility, you ensure that your financial foundation remains resilient, regardless of the broader economic environment.

Ultimately, your journey toward financial independence relies on your ability to manage both the growth of your total assets and the accessibility of your funds. By focusing on your liquid net worth, you empower yourself to navigate economic uncertainties without compromising your long-term goals. Use this metric as a compass to ensure that you are not just building wealth on paper, but also creating the tangible flexibility required to live life on your own terms. Whether you are building an emergency fund or adjusting your investment strategy, keep your focus on maintaining that critical layer of liquid capital. It is the best form of insurance for your personal financial future.

Related Terms:

- net worth calculator

- liquid net worth by age

- liquid net worth chart

- liquid net worth percentiles

- average liquid net worth

- Personal Net Worth